The 3-NDFL tax return is filled out by the taxpayer using the form approved by the Federal Tax Service (Order of the Federal Tax Service of Russia dated October 3, 2018 N ММВ-7-11/569@ "On approval of the tax return form for personal income tax (form 3-NDFL ), the procedure for filling it out, as well as the format for submitting a tax return for personal income tax in electronic form").

Form 3-NDFL for 2017:

What is the fastest and easiest way to get the correct 3-NDFL declaration?

The easiest way is to quickly prepare the correct 3-NDFL declaration with Tax. With Taxation, your declaration will not have to be redone. The tax office will generate the necessary sheets of the form, calculate the totals, enter the necessary codes and check the data. You will receive the correct declaration and expert advice. And then you can choose whether to take the declaration to the inspectorate yourself or submit it online.

For 2016:

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Federal Tax Service (Order of the Federal Tax Service of Russia dated November 25, 2015 No. ММВ-7-11/544@). You can download it by following the link above (source - Federal Tax Service).

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Federal Tax Service (Order of the Federal Tax Service of Russia dated December 24, 2014 No. ММВ-7-11/671@). You can download it by following the link above (source - Federal Tax Service).

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Federal Tax Service (Order of the Federal Tax Service of Russia dated November 10, 2011 No. ММВ-7-3/760@ as amended by Order of the Federal Tax Service of Russia dated November 14, 2013 No. ММВ-7-3/501@) . You can download it by following these links above (source - Federal Tax Service).

The tax return is filled out and printed according to certain rules. These rules are established by the Federal Tax Service (order of the Federal Tax Service of Russia dated November 14, 2013 No. ММВ-7-3/501@). You can download instructions for filling out form 3-NDFL by following this link.

For 2012:

For 2011:

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Federal Tax Service (Order of the Federal Tax Service of Russia dated November 10, 2011 No. ММВ-7-3/760@). You can download it by following this link (source - Federal Tax Service).

The tax return is filled out and printed according to certain rules. These rules are established by the Federal Tax Service (order of the Federal Tax Service of Russia dated November 10, 2011 No. ММВ-7-3/760@). You can download instructions for filling out form 3-NDFL by following this link.

For 2010:

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Federal Tax Service (Order of the Federal Tax Service of Russia dated November 25, 2010 No. ММВ-7-3/654@). You can download it by following this link (source - Federal Tax Service).

The tax return is filled out and printed according to certain rules. These rules are established by the Federal Tax Service (order of the Federal Tax Service of Russia dated November 25, 2010 No. ММВ-7-3/654@). You can download instructions for filling out form 3-NDFL by following this link.

For 2009:

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Ministry of Finance (Order of the Ministry of Finance No. 145n dated December 29, 2009). You can download it by following this link (source - Federal Tax Service).

The tax return is filled out and printed according to certain rules. These rules are established by the Ministry of Finance (Order of the Ministry of Finance No. 145n dated December 29, 2009). You can download instructions for filling out form 3-NDFL by following this link.

For 2008:

Tax return 3-NDFL is filled out by the taxpayer using the form approved by the Ministry of Finance (Order of the Ministry of Finance No. 153n dated December 31, 2008). You can download it by following this link (source - Federal Tax Service).

The tax return is filled out and printed according to certain rules. These rules are established by the Ministry of Finance (Order of the Ministry of Finance No. 153n dated December 31, 2008). You can download instructions for filling out form 3-NDFL by following this link.

This article will provide step-by-step instructions for filling out the 3-NDFL declaration in 2019. Taxpayers will be able to find out what sheets the declaration submitted for verification should consist of, how the document is filled out, as well as some important details that must be taken into account in order to receive an income tax refund for an apartment.

- on form 3-NDFL for 2017.

- for a completed tax return.

- for the 2016 program for registration of 3-NDFL.

Individuals who want to reduce their tax base due to spending money on purchasing an apartment can print it out, enter the required information into it, send it for verification and soon receive a deduction. However, the document form must be used in a strictly defined form (put into effect on December 24, 2014 using order number MMV-7-11/671).

Attention! Before you start processing 3-NDFL for personal income tax reimbursement for an apartment, we advise you to read article number 220 of the Tax Code of Russia, which will help the taxpayer make sure that he can actually receive according to the law, or, on the contrary, understand that he does not have this right .

What sheets to draw up

An individual will need to indicate data on the title page of form 3-NDFL, on the sheet entitled information on tax amounts subject to refund from the budget (this is section number one), on the page requiring information about the size of the taxable base (this is the second section) , as well as on sheets A and D1.

Sheet A is intended to enable an individual to report in writing to the tax authority on his income received from sources located on the territory of the Russian Federation. Therefore, if a taxpayer’s profit is transferred to his bank card from other countries, then he must fill out Sheet B.

Sheet D1 is devoted to calculation data regarding property deductions that are provided in the case of the purchase of real estate, including an apartment. Otherwise, if the taxpayer sold the property, he is required to fill out sheet D2 instead of sheet D1.

Instructions for filling out sheet D1

When returning an apartment tax, there is no way to do without completing Sheet D1. To make this process as quick and easy as possible, we recommend using the instructions below:

- We provide the details. An applicant for a property deduction must write the numbers of his identification number at the top of the page, then number the sheet itself (numbering starts with two zeros, that is, if this is the fifth page, then you need to write “005”), and then indicate your last name along with initials .

- We enter the codes. First of all, this is the object name code. In the case of a tax refund for an apartment, you need to put the number two. It is also necessary to enter the identification of the taxpayer (if the applicant for a tax discount is the owner of real estate, then the code “01” is entered). And the last cipher required is the region code. Each region of the Russian Federation has its own numerical codes. For example, for the Moscow region the code is “50”, for the Rostov region - “61”, and for the Volgograd region - “34”.

- We note the type of property and paragraph of Article 220. Subclause 1.3 provides the taxpayer with four options for forms of ownership, from which he must choose one. For example, if an individual claiming a deduction has registered an apartment in the name of his son, who is not yet eighteen years old, then the number four is selected, and if the property entirely belongs to the taxpayer - one. Then in subparagraph 1.4 you need to indicate whether this declaration is related to the tenth paragraph of Article 220 or not.

- We indicate the address of the apartment. First of all, the numbers that make up the postal code are entered. Then write the names of the city and street where the apartment is located. Each of these names must be written in capital Russian letters. And after that, the taxpayer just has to put down the house and apartment numbers.

- We indicate the dates for receipt and submission of some documents. The current legislation has adopted a rule stating that until an individual completes the stage of registering ownership of a property, he will not be awarded property compensation. Therefore, in subclause 1.7 it is required to indicate the date of registration of this right. And in subclause 1.9 indicate the day, month and year when the taxpayer submitted an application for a tax discount for the apartment.

- We display the amount of expenses. Subclause 1.12 states the amount that an individual spent to purchase an apartment. However, the indicated value of this real estate property should not exceed the maximum possible amount from which a deduction can be calculated (this is two million rubles). That is, if an apartment costs nine million, then you only need to write two million in this paragraph.

- We calculate the tax base. In paragraph 2.7, an individual must indicate the figure that he will get when subtracting the provided property discount from the total amount of income he received during the tax period. Then in paragraph 2.8 you need to note the amount of expenses, prescribed based on the cost of the apartment fixed in the purchase and sale agreement.

- We write down the amount of the remaining deduction. Since an individual, by law, cannot withdraw from the state budget in a year more than the personal income tax he contributed during the same period, the issuance of property compensation is extended over several years. Thus, if the maximum amount of the tax discount is declared in the declaration, and the annual amount of the deduction is 600,000 rubles, then the balance will be equal to 1,400,000 rubles.

It should be noted that if the 3-NDFL form for a property tax discount is drawn up on behalf of the wife/husband of the apartment owner, then the taxpayer’s attribute code is no longer “01”, but “02”. If the parents of a minor owner want to reimburse the tax - “03”, if an individual owns the property on an equal basis with the child - “13”, and if the apartment belongs simultaneously to the taxpayer, his child and spouse - “23”.

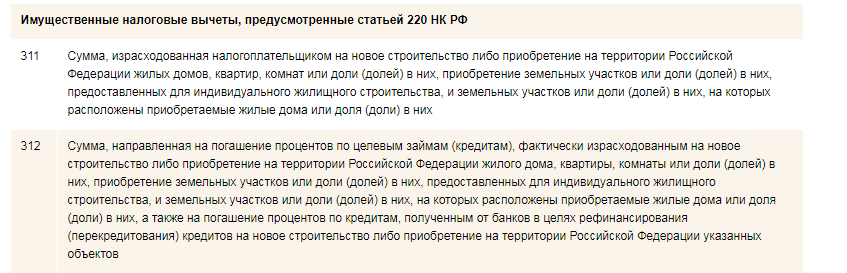

Code 311 in the declaration

We propose to dwell on such a nuance as code 311 in the tax return. Individuals will encounter it if they choose the software method.

As you know, a certificate in form 2-NDFL is attached to the tax return. This certificate contains all kinds of information about the income of an individual, tax charges collected from them and the deduction code in question.

Tax deductions of the property type are coded only by two numerical combinations - these are 311 and 312. The first code is indicated on the declaration form if an individual spent money either on the acquisition or construction of a real estate property. And code 312 is used in situations where the taxpayer spent money to repay interest accrued on a loan taken for the purpose of purchasing or constructing a property.

Important! Do not forget to put a signature at the bottom of each page of the declaration and indicate the date to the right of it, since without this the document will not have legal force.

To fill out the declaration, go to the section "Life Situations" Choose a section - “Submit 3-NDFL declaration”, then button “FILL OUT A NEW DECLARATION ONLINE.”

An example of filling out Form 3-NDFL in the “Taxpayer’s Personal Account”

An example of filling out Form 3-NDFL in the “Taxpayer’s Personal Account”

Select the year for which the tax return is being prepared. (In your personal account, you can fill out a declaration only for yourself).

The fields “Last name”, “First name”, “Patronymic name”, “TIN” will be filled in automatically.

If you indicate the TIN, then information about the date and place of birth, citizenship, and identity document do not need to be entered. If you do not have a TIN, these sections are required to be completed.

An example of filling out Form 3-NDFL in the “Taxpayer’s Personal Account”

An example of filling out Form 3-NDFL in the “Taxpayer’s Personal Account”

2. Choice of income

Select the income you want to declare in your declaration and click the "NEXT" button.

3. Choice of deductions

A tax deduction is an amount that reduces the amount of income on which tax is levied, or allows you to return part of the tax previously paid to the budget.

Select the deductions that need to be included in the return and click the "NEXT" button.

4. Filling out the “Income” section

In the “Income” section, by default the tab “Income taxed at a rate of 13%” is available for entry.

To enter income, click the “Add Income” button.

If you need to enter other income, select the appropriate interest tab.

4.1 According to the 2-NDFL certificate, enter the following data:

- “Source of income” - INN, KPP, name of the organization and code “OKTMO”;

- Enter Information about the income received. If necessary, you can indicate several incomes taxed at the specified rate from a given source. If you are transferring data from a 2-NDFL certificate, you only need to enter each type of income once, indicating the total amount of income of this type.

4.2 When filling out a declaration in connection with the sale of property (apartment, land, etc.) owned for less than 3 years:

In the “Information about income received” section, enter:

Select Revenue Code:

- when selling an apartment, garden house and land - “1510”;

- when selling a share of an apartment - “1511”;

- for the sale of vehicles, garages, unfinished construction projects - “1520”.

Enter the amount of income received from the sale of the property.

Select deduction code:

- when selling an apartment, garden house and land - “901” (1,000,000 rubles) or “903”

(in the amount of documented expenses);

- when selling a share of an apartment - “904” (amount equal to 1,000,000 rubles / share) or “903” (in the amount of documented expenses);

- when selling a vehicle, garage, unfinished construction project - “906” (250,000 rubles) or

“903” (in the amount of documented expenses). Enter the deduction amount.

If all income has been entered, click the “Next” button.

5. Filling out the “Deductions” section.

5.1 To receive property tax deductions In the “Property tax deduction” tab, enter data on expenses for the purchase of housing and repayment of interest on targeted loans.

Enter data on the object using reference books.

Depending on whether you are receiving a property deduction for the first time or whether you have already received part of the deduction previously, fill out the form in the “Total expenses” block.

5.2 If you additionally want to receive a social tax deduction, select the appropriate tab in the deductions menu.

To receive social tax deductions, check the appropriate box.

Enter the amount of expenses in the appropriate line.

To receive tax deductions, you must provide documents confirming expenses to the tax office. You can send electronic images of documents through your personal account; to do this, scan the documents before sending the declaration.

Click the “Attach document” button, select the location of the document file - the “Select file” button. In the “Description” line, enter brief information about the document (for example, an income certificate) and click the “Attach file” button.

6. View the generated declaration

After filling out all the necessary sections, the “Results” form opens, which displays the results of filling out the declaration.

To edit data, you can enter any section of the declaration.

To see what the declaration looks like on paper, click the “View generated declaration in pdf format” button.

To view the declaration, you must have Adobe installed on your computer.

Reader".

After all documents that require sending have been saved, in the “Sign with a key of an enhanced unqualified electronic signature” section, enter the password that you entered when you generated the electronic signature certificate and click the button “Confirm and send.”

If you have forgotten your password, you can generate a signing certificate again by revoking the current certificate.

Once sent to the inspection, the declaration cannot be edited, but if necessary, you can

fill out the updated declaration and send it to the inspectorate.

8. Filling out a tax refund application

If you submit a declaration in order to receive a tax deduction, you must also send an application for a tax refund to the inspectorate.

To do this, in the “Results” section of the “Filling out and electronically submitting the 3-NDFL tax return” section, select the “Refund/Payment of Taxes” tab and click the “Refund Application” button.

Fill in the required information and click the “Save and Continue” button.

To send the application to the inspection, enter the password that you entered when you generated the electronic signature certificate and click the “Submit” button.

After sending the application in the “Results” section, the message “The document was

received and registered with the inspection.”

In addition, information about registering an application can be seen in the “Taxpayer Documents/Electronic Document Flow” section.

9. Sending a declaration completed in the “Declaration” program

If you filled out a declaration in the “Declaration” software product or other software that generates an xml file, then it can be sent to the inspectorate from your personal account.

In the same thread “Filling out and electronically submitting the 3-NDFL tax return,” instead of the “FILL OUT A NEW ONLINE DECLARATION” button, click on the “SEND DECLARATION COMPLETED IN THE PROGRAM” button.

An example of filling out Form 3-NDFL in the “Taxpayer’s Personal Account”

An example of filling out Form 3-NDFL in the “Taxpayer’s Personal Account”

Select the declaration year and file. Attach supporting documents, sign with an electronic signature and send the declaration to the inspectorate. If you submit a return to obtain a tax deduction, do not forget to submit a refund application.

10. Obtaining a tax deduction from the employer

You can receive a tax deduction before the end of the tax period by contacting your employer,

having previously confirmed this right with the tax authority. Application for Confirmation of Eligibility

The tax deduction can be filled out in your personal account and sent to the tax office by signing with an electronic signature.

To fill out an application, in the “Life Situations” tab, select the “Request a certificate and other documents” section, then select the required certificate.

In the window that opens, fill in the required data, attach electronic copies of documents, sign with the electronic signature key received in your personal account, and click the “Submit” button.

After 30 days, receive a notification from the tax authority about the right to a property deduction and give it to your employer.

Filling out an income tax return using special software is the second most popular preparation for 3-NDFL to obtain a tax deduction. Let us consider in detail how to fill out 3 personal income taxes in the “Declaration.2017” program when applying for expenses for purchasing an apartment or building a house.

Step-by-step instructions for filling out 3-NDFL using the “Declaration.2017” software

Step 1. Install and run the program

You can download the “Declaration” program for filling out 3-personal income tax for 2017, 2016, 2015 and 2014 on the website of the Federal Tax Service or the State Scientific Research Center.

In the window that opens, we immediately go to the first tab “Setting conditions”.

Please note that some of the conditions have already been established (type of declaration, type of income and taxpayer attribute) and no need to change them.

Step 2. Fill in the first tab “Set conditions”:

Inspection number

You can find out which inspection you are attached to using the service “Determining the details of the Federal Tax Service, the state registration body of legal entities and/or individual entrepreneurs serving a given address,” located on our website. To do this, you must indicate the address of residence (registration according to your passport). There is no need to fill in the “Inspectorate Tax Code” field.

Correction number

We do not touch this field. “1” is set only if an updated tax return is submitted, in which errors in the previously submitted and accepted for verification declaration are corrected.

OKTMO

This field does not need to be filled in; it will be filled in automatically after specifying the OKTMO of the employer.

When applying for a deduction, the employer's OKTMO is indicated, and when paying personal income tax on income received from the sale of property, the employer's OKTMO of the place of permanent registration is indicated.

This completes filling out the “Setting Conditions” tab.

If the declaration is filled out and submitted by a representative, you must fill out the block “Reliability confirmed”, where you should indicate the full name of the representative and details of the power of attorney on the basis of which he acts.

Step 3. Fill out the second tab “Information about the declarant”

This section must be filled out in exact accordance with the passport, otherwise the tax authority may refuse to accept the declaration.

Tab "Code of the country" no need to change.

Step 4. Fill out the third tab “Income received in the Russian Federation”

In this section you need to indicate the sources of income received in the year for which the deduction is claimed.

To do this, next to the block “Payment sources”, click on the green plus sign. In the tab that opens, indicate the name of the employer, his INN/KPP and OKTMO. All this information can be taken from the 2-NDFL certificate.

If, along with a property deduction, is declared at the same time, then in the tab that opens, you must put a tick next to the line “Calculate standard deductions using this source”.

You can check or correct the entered information about the source of income by clicking on the button indicating a hand pointing to a notepad, and you can delete the data by clicking on the red minus sign.

Step 5. Deposit the amount of income received monthly

To do this, click on the green plus in the second block of the section and select the type of income received by clicking on the button “Revenue code”.

For salary under an employment contract, select the code “2000 – Wages and other income in pursuance of an employment contract”, for income under GPC agreements - code “2010 – Work under civil contracts”.

Then we indicate the amount of income and the month it was received.

It is better to take the income code, amount and months of receipt from the 2-NDFL certificate.

If your income has not changed during the year and every month you received the same amount (according to the 2-NDFL certificate), you can use the button “Repeat income”.

Then in the lines below we indicate the taxable amount of income (line “Tax base” in the 2-NDFL certificate), the amount of tax calculated and withheld.

We do not fill in the last line “Advance payments of a foreigner”.

An example of a correctly completed “Income received in the Russian Federation” tab:

Step 6. Proceed to filling out the “Deductions” tab

By default, the program takes us to the “Standard Deductions” tab. If you do not plan to receive a standard deduction along with the apartment deduction, check the box “ Provide standard deductions” remove and go to the tab "Property".

Then check the box “Provide a property tax deduction” and click on the green plus sign to add data about the purchased apartment for which the deduction will be claimed.

Step 7. Enter data about the purchased apartment into the program

Method of purchasing real estate: under a purchase and sale agreement (when purchasing a finished apartment) or investment (when purchasing a new building).

Object name: residential building, apartment, room, joint venture with a residential building or for individual housing construction, shares in the specified property.

Type of property:

- Individual- if the apartment is purchased as sole property.

- Total share- when buying an apartment in share with someone (usually in marriage when dividing a share in the apartment between spouses and their children, or between a parent and a child).

General joint with a statement on the distribution of expenses- when purchasing housing during marriage without allocating shares (50% for each spouse).

This type of property is indicated if the entire amount of the deduction is claimed by one of the spouses, and the other refuses it, or in the case when both spouses receive a deduction in the shares established by them.

General joint without a statement on the distribution of expenses- this type is indicated if the cost of housing exceeds 4 million rubles and an application for distribution of expenses is not required, since the maximum amount of deductions that each spouse can declare is no more than 2 million rubles, and redistribute it by giving it to the second spouse so that he declares a deduction of not 2 million rubles, but 4 million rubles. - it is forbidden.

Also, an application will not be required if one of the spouses declares it in the amount of 50%. This is due to the fact that the deduction for the common joint property of the spouses is distributed by default in the ratio of 50% to 50%.

Common shared ownership with a statement on the distribution of expenses- this type of property is indicated when spouses want to distribute the deduction in a proportion different from the shares they own. As a rule, this happens if one of the spouses does not work and cannot receive his share of the deduction, or the income of the second spouse allows him to receive the deduction immediately.

The spouses received the right to distribute the deduction when purchasing an apartment in shared ownership only in 2014. deduction will be given only in accordance with the shares in the property.

Taxpayer identification:

- Owner of the object- if the deduction is claimed when purchasing an apartment as sole property.

- Property owner's spouse- indicated when applying for a deduction for the purchase of an apartment during marriage (regardless of the type of ownership: shared or joint).

- Parents of the minor owner of the property- if the deduction is claimed by the owner of the apartment.

- The property is owned by the applicant and a minor child- if the apartment is registered as the property of the parent together with the child.

- The property is owned by the applicant’s spouse and child- if the apartment is registered as the property of both parents and the child (children).

Object number code:

If the purchased property has a cadastral, conditional or inventory number, it must be entered in the line “Object number”, before indicating the code of the object number.

Location:

We also indicate the location address from the USRN extract or from the Rosreestr website.

At the end we indicate the date of the document confirming the right to deduction. For a purchase and sale agreement, you must fill out the line “Date of registration of ownership rights to a residential building, apartment, leasehold”. For investment agreements - date deed of transfer of an apartment, room or share in them.

Year of start of using the deduction:

If the deduction is claimed for the first time, indicate the year “2017”; if it was declared in previous years, indicate the year when the very first declaration for the deduction was submitted.

If you are a pensioner, do not forget to check the box “I am a pensioner”. You can learn about the features of receiving deductions for pensioners from.

Cost of the object (share):

We indicate the full cost of the apartment for which the deduction is claimed. If there was an apartment, you can also indicate the amount of interest paid.

This completes the filling of the “List of Objects” block.

Strings “Deduction from a tax agent in the reporting year (code 311) and (code 312) are filled out only if they are indicated in the 2-NDFL certificate in the section 4. Standard, social and property tax deductions.

This completes filling out the declaration. At the very end, we select the action that we want to apply to the declaration: save, view, print or check.

The text of this article will be useful to those taxpayers who want to know how to fill out the property deduction for the 3rd year.

Download a sample 3-NDFL declaration form for property deduction for the 3rd yearIn order for the tax refund procedure for the purchase of real estate to be successful, we strongly recommend taking into account the rules for preparing a tax return, which will also be discussed.

- declarations for 2017.

- Form 3-NDFL to receive a deduction for the purchase of property.

- Special for filing a tax return.

As is known, compensation that is accrued to taxpayers who have invested material resources in the acquisition or construction of property assets is the largest in size compared to other types.

Since tax legislation has adopted a rule stating that an individual can return no more money in a year than he contributed to the state budget for income tax, the payment is usually extended over several years.

It should be noted that to receive all the funds accrued as a deduction for the purchase of property, submitting Form 3-NDFL once is not enough. The taxpayer should enter data into the declaration form every year, submit it for review to the tax service and thus gradually withdraw the property compensation due to him.

First pages of the declaration

Before indicating information related to the purchased housing or land plot, the taxpayer must enter information about his income, as well as display some information about himself. This is done using the first four sheets of the 3-NDFL form - the title, the first section, the second, as well as sheet A and/or B, the last of which is intended to be filled out by individuals receiving funds from foreign sources of profit.

Basically, however, they also contain several of the following meanings, which not all applicants for property deductions know how to work with:

Sheet D1

After the buyer of the property completes the main pages of the declaration, he will need to work with sheet D1. It is on this page of form 3-NDFL that you need to calculate property tax compensation and provide some general information. An individual will need to provide the following information:

- Code of the purchased property. Since you can get a deduction not only for a house or apartment, but also for other property objects, it is necessary to note what kind of real estate was purchased. If this is a house with a plot of land attached, then the code in this case is 7, if the apartment is 2.

- Sign of an applicant for deduction. In order to indicate how many owners own the property for which a tax discount has been applied for, as well as which of them applies for it, a taxpayer attribute code has been invented. Thus, if an individual who is the sole owner of the house wants to take advantage of the deduction, then he needs to write the numbers 01.

- Object data. Also, the taxpayer must indicate whether he owns the acquired property individually or whether the property is registered as a shared or joint property, write the full address where this property is located, and also indicate the date of registration of the right to the property and the date of filing for the distribution of property tax compensation.

- Various amounts. First of all, the buyer of the property is required to display the amount he spent on its purchase, and then the amount (this action is necessary if a loan was taken out). In addition, the size of the tax base is entered, from which property tax compensation has already been deducted, and the amount of costs recorded in documents is written down.

- Remaining deduction. Since we are talking about receiving property-type compensation for the third year, it is very important to correctly fill out the cell that implies indicating the residual tax credit. An individual needs to take the declaration for the previous year and subtract the amount of the deduction that will be provided to him for the current tax period from the balance recorded in it, and reflect the result obtained in line 230 of sheet D1.

How to get a tax refund on mortgage interest payments

Since a loan is a fairly popular service that makes the process of purchasing real estate quite easy, borrowers take advantage of this and charge individuals considerable interest.

However, it is also provided for in current legislation. Costs of this kind must be included in the corresponding lines of sheet D1 - 130 and 240.

The main thing is to keep separate records of expenses associated with the purchase of property and the payment of interest, and in no case add them up.

Thus, in paragraph 1.13 the amount that the deduction applicant has currently spent on paying off interest and has not received compensation for it is entered, and in paragraph 2.11 - the balance of the tax rebate due for interest expenses to the taxpayer in the future.

Important! All amounts declared by an individual in sheet D1 must be indicated on the basis of declarations for or be confirmed using other documentation of a settlement nature.